Pastor Taxation – Dual Status

- Crawford Ulmer

- Dec 11, 2025

- 3 min read

There are some unique tax situations that apply to pastors:

Their “dual status” as it relates to federal income tax and self-employment tax.

Housing allowance.

The accounting for these unique situations can be a burden for pastors, particularly because many pastors may not have the knowledge of the unique rules that apply to them. Also, especially at small churches, there may not be another paid pastor who can point them in the right direction.

This article will just cover pastors’ “dual status,” but I will plan to write a future post about the housing allowance.

How FICA works for most employees

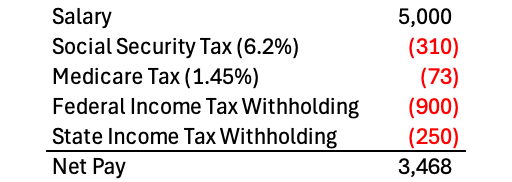

Almost all employees are subject to FICA, or Social Security and Medicare taxes. They have FICA withheld from their paycheck and their employer also pays the employer side of FICA. Employees will also have federal and state income tax withheld from their paychecks as well. A paycheck for a “normal” employe may look something like this:

As mentioned above, there is also the employer side of FICA. So in this case, the employer is paying $310 + $73 = $383 in FICA as well.

Pastors do not pay FICA

Pastors and their churches cannot pay FICA, like “normal” employees/employers. Instead, pastors are considered self-employed for Social Security and Medicare tax purposes. As such, they are subject to self-employment tax (SECA), where they pay the equivalent of both the employee and employer portions of Social Security and Medicare taxes. For more information, you can read this article I wrote several months ago about self-employment tax.

Even though pastors are considered self-employed for Social Security and Medicare tax purposes, they can still be considered employees for income tax purposes. This is how they are "dual status" – employees for income tax purposes, but self-employed for Social Security and Medicare tax purposes.

As employees, they receive a W2 from the church they work for, but it will show $0 for the Social Security wages and withholdings (boxes 3 & 4) and $0 for the Medicare wages and withholdings (boxes 5 & 6). For more information about W2s, you can read this post from a couple of years ago about understanding your W2.

Instead of the Social Security and Medicare tax being calculated and paid by the employer, the pastor will calculate and pay it themselves on Schedule SE, which is a form that is part of their tax return.

Pastors are required to pay self-employment tax on their housing allowance as well.

It is important to note that this treatment applies to "ministers" and does not generally apply to other church staff. The IRS has specific language about who qualifies as a minister. According to the IRS, a minster is someone who is ordained, commissioned, or licensed by a religious body, such as a church or denomination. Ministers may conduct worship, perform sacerdotal functions, administer ordinances, or maintain religious organizations.

History behind this odd set-up

Although I have understood the unique dual status of pastors for some time, I have always been curious why it is set up this way. Not everything in regards to our tax system makes sense, but it turns out that there is a decent explanation.

In doing research, I’ve found the following:

Ministers were initially excluded from Social Security when it was created, along with other groups of workers.

Ministers were later allowed to voluntarily opt-in to be part of the Social Security system.

If ministers were at one point individually opting-in, it makes sense that they would use the form that self-employed people use to pay these taxes individually.

It was subsequently changed so that all ministers would be covered, unless they opt-out. Ministers can still opt-out today.

Also, according to an article published by the Social Security Administration, churches thought that being required to collect taxes for the government would interfere with the separation of church and state – this is an interesting rationale to consider. Pastors paying the Social Security and Medicare taxes individually on their tax return, like a self-employed person, means that the church does not have to be involved with the government program.

How does this relate to your situation?

If you are interested in discussing pastor taxation further or any other part of your tax situation, feel free to schedule a meeting or contact me via email (crawford@ulmerfinancial.com).

I bring together clients’ investments and tax preparation in one place, so they don’t have to deal with multiple advisors. The goal is to make managing your money and filing your taxes easier.

Comments